Buying a property is one of the biggest financial decisions you’ll make, and there isn’t a one-size-fits-all answer to “what age is right?” The ideal time depends on your personal financial circumstances, long-term goals, and market conditions. In this post, we’ll explore the factors that influence the best age to buy a home in the UK, supported by authentic data and expert advice.

Average Age of First-Time Buyers in the UK

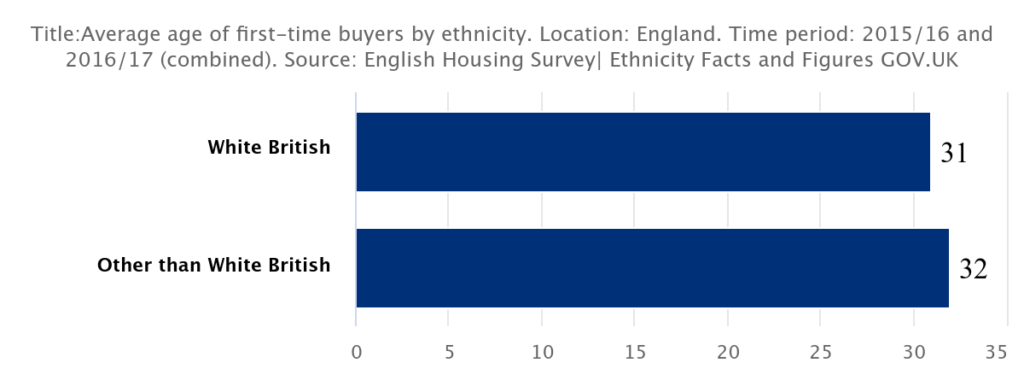

According to UK Finance, the average age for first-time buyers in the UK is around 34 years old. Rising property prices, higher deposit requirements, and changing career paths mean that many people are entering the property market later than in previous generations.

Factors to Consider When Deciding the Right Time to Buy

When determining if now is the right time for you, consider these key factors:

Financial Stability:

• Do you have a stable income and a good credit score?

• Are you able to save for a deposit (often 10–20% of the property price)?

Mortgage Eligibility:

• Lenders assess affordability based on your income and outgoings. Use a mortgage calculator to get an idea of what you can afford.

Market Conditions:

• Are property prices trending upward or downward in your preferred area?

• Research local listings on Rightmove or Zoopla.

Government Schemes:

• Schemes like Shared Ownership, First Homes, and Lifetime ISAs can help make buying a home more affordable.

Buying a Home in Your 20s: Early Start, Long-Term Gains

Pros:

• Time Advantage: A longer mortgage term (often 25–35 years) means lower monthly repayments.

• Equity Growth: You have many years to build equity as property values appreciate.

Cons:

• Limited Savings: Early in your career, saving for a deposit can be challenging—especially if you’re managing student loans or starting salaries.

• Financial Instability: Income fluctuations may make lenders cautious.

Buying a Home in Your 30s: The Most Common Age

Pros:

• Financial Maturity: By your 30s, you’re likely to have a higher earning potential and some savings accumulated, making it easier to meet deposit requirements.

• Stable Career: A stable job history helps in securing a favorable mortgage rate.

Cons:

• Market Competition: As more people in their 30s look to buy, competition can drive prices higher, especially in urban areas.

• Rising Prices: Compared to your 20s, you might face higher property prices due to market inflation.

According to Which?, the 30s are the most common time to purchase a property, as many individuals balance family planning with long-term investment goals.

Buying a Home in Your 40s & 50s: More Stability, but Different Challenges

Pros:

• Greater Savings: By your 40s or 50s, you’re likely to have more substantial savings or equity from previous property ownership, allowing for a larger deposit or even a move to a better property.

• Investment Opportunities: With financial stability, you might consider investing in a second property or upsizing.

Cons:

• Shorter Mortgage Terms: Lenders may offer shorter mortgage durations, resulting in higher monthly payments.

• Retirement Considerations: You must weigh home affordability against retirement planning needs.

Final Thoughts

There isn’t a universally “perfect” age to buy a property in the UK—it’s all about when you are financially and personally ready. Whether you’re in your 20s, 30s, or beyond, planning ahead and understanding your financial situation is key to making a well-informed decision.

Ready to take the plunge? Start by evaluating your finances, researching your local market, and exploring government schemes that might be right for you. Remember, your journey to homeownership is unique—make sure it aligns with your long-term goals.

Great post

Good information!